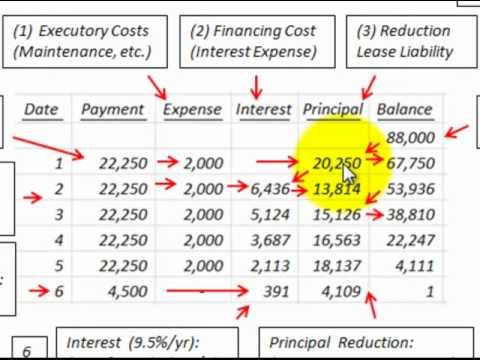

All this can be helpful for issues like tax deductions for curiosity funds. An amortization schedule is a table that chalks out a loan repayment or an intangible asset’s allocation over a specific time. It breaks down every payment or expense into its principal and interest components and identifies how much every aspect reduces the excellent balance or asset value.

The amortization schedule usually contains the payment date, cost amount, interest expense, principal repayment, and excellent balance. It aids the debtors and lenders in monitoring the loan reimbursement’s progress and attracts a clear image of how the principal and curiosity portions change over the mortgage or asset’s lifespan. Loan amortization breaks a mortgage balance into a schedule of equal repayments based on a particular loan amount, mortgage term and rate of interest. This loan amortization schedule lets debtors see how a lot curiosity and principal they’ll pay as a part of every month-to-month payment—as well because the outstanding steadiness after each fee. Amortization is the strategy used to allocate the price of intangible property https://www.simple-accounting.org/ over their helpful life, while depreciation applies to tangible, fastened property to account for their put on and tear over time.

The term can also discuss with the method of spreading out the worth of an intangible asset over its helpful life. Understanding amortization on this context helps in managing money flows, as it presents predictable monthly funds that cover both the principal and interest. It additionally aids in long-term strategic planning, permitting companies to forecast when main expenses like refinancing or property upgrades shall be viable.

Accounting Skills In On An Everyday Basis Life

- This implies that this firm would report an expense of $10,000 yearly.

- This might help to provide a extra correct picture of the true value of the asset, in addition to to guarantee that expenses are properly accounted for over time.

- Understanding amortization on this context helps in managing cash flows, because it provides predictable monthly payments that cowl both the principal and interest.

- Mounted funds over time can result in general financial savings in curiosity compared to different mortgage sorts, providing a structured reimbursement schedule that aids in monetary planning.

Amortization pertains to intangible belongings like patents and copyrights, allocating their value evenly over a predetermined timeframe. Depreciation, then again, applies to tangible belongings, such as equipment and buildings, and infrequently makes use of numerous strategies like straight-line or declining balance to replicate their wear and tear. Amortization applies to intangible belongings by spreading their price over their helpful lives, acknowledged in equal installments on a company’s monetary statements. For instance, if your corporation acquires a patent legitimate for ten years at $10,000, you’d amortize $1,000 annually. This approach systematically reduces the asset’s guide worth over time and reflects its consumption or use.

The month-to-month funds stay fixed throughout the life of amortized loans except you modify the mortgage terms or refinance the mortgage. Amortized loans are typically paid off over time with equal funds in every period. Amortized loans have an amortization schedule during which a portion of every fixed month-to-month cost comprises the monthly interest and the principal mortgage balance. An amortized loan involves frequently scheduled funds, with each fee overlaying each interest and principal. Initially, funds are interest-heavy, but over time, they gradually favor the principal.

Mortgage amortization is the method of paying off a home mortgage over time through common funds. Every fee contains each principal and curiosity, progressively decreasing the general mortgage stability till it’s totally paid off by the top of the mortgage term. By amortizing the value of an intangible asset, a enterprise can cut back its taxable revenue over a number of years, rather than taking a large expense in a single yr.

A portion of each installment covers curiosity and the remaining portion goes towards the loan principal. The easiest method to calculate payments on an amortized loan is to use a mortgage amortization calculator or table template. Nevertheless, you’ll have the ability to calculate minimum payments by hand using simply the mortgage amount, rate of interest and mortgage term. Debtors can make additional funds to minimize back the principal, but monthly payments keep the identical. In different words, paying additional on an amortized loan reduces the loan balance, shortens the mortgage time period, and saves you interest, however it does not change the month-to-month fee. A widespread instance of loan amortization is a mortgage, where month-to-month funds are made in equal amounts, masking both curiosity and principal over the mortgage period.

Amortization: What Are Amortized Loans And Why Must You Care?

When an asset turns into obsolete, its useful life is shortened, and its amortization schedule might need to be adjusted accordingly. Loan funds are used to repay the principal and curiosity of the loan. By understanding how this course of works and the way it can be utilized in numerous situations, you can even make more informed monetary decisions and make certain that your bills are correctly accounted for. We can simply work out the amortization of the tv alongside its 10-year helpful life. One of the commonest calculations is annual amortization, the place we divide the initial cost of the asset by its estimated useful life (EUR 1,000/10 years). In the first year, it’ll have amortized EUR a hundred; in the second, EUR 200; and in the third, EUR 300, and so forth until we attain the quantity we paid.

Amortization Schedules

Professional guidance ensures effective navigation of complicated amortization processes, enhancing general monetary administration. The double declining stability method accelerates depreciation by applying double the straight-line rate to the asset’s remaining book value. This technique allows for early expense recognition, which can be advantageous for tax purposes and financial planning. The straight-line method is considered one of the easiest and most commonly used strategies of amortization. It entails spreading the value of an asset evenly over its helpful life, leading to equal expense quantities each interval.

These repayments are typically made over a pre-arranged time period and are made until the loan’s balance hits zero. Amortization presents a quantity of benefits and drawbacks that must be thought of. It is used to claim the capital value allowance on long-term assets and could be essential for monetary planning and tax optimization.

As the loan matures, more and more of the fee quantity goes towards paying down the principal stability. Amortization is an accounting time period that’s used in two different (and unrelated) areas. In the first case, amortization is a process the place you spread the value of a specific asset over its useful life. The second use of the word amortization (arguably rather more frequent, especially if you’re not a enterprise owner) refers back to the method that loan payments are spread out over the course of a loan. It Is important to know how amortization works and how it compares with depreciation, which is a similar term. Amortization aids financial planning by permitting borrowers to pay down debt by way of common curiosity and principal payments.